Abstract: According to the latest research forecast from global technology intelligence company ABI Research, the global market size of basic robot models driven by Physical Artificial Intelligence (PAI) technology will reach $150 billion by 2036. The underlying driving force behind this leapfrog growth lies in the fact that this technology has completely broken through the "rigid control bottleneck" of traditional control engineering. This article will take an operational technology (OT) and factory field practice perspective to deeply analyze the generalization capabilities of basic models, the real-time game of edge computing stacks, and the clear ROI delivery path in controlled industrial environments.

I. Introduction: Rigid Control Bottlenecks and the Control Challenges of Unstructured Environments

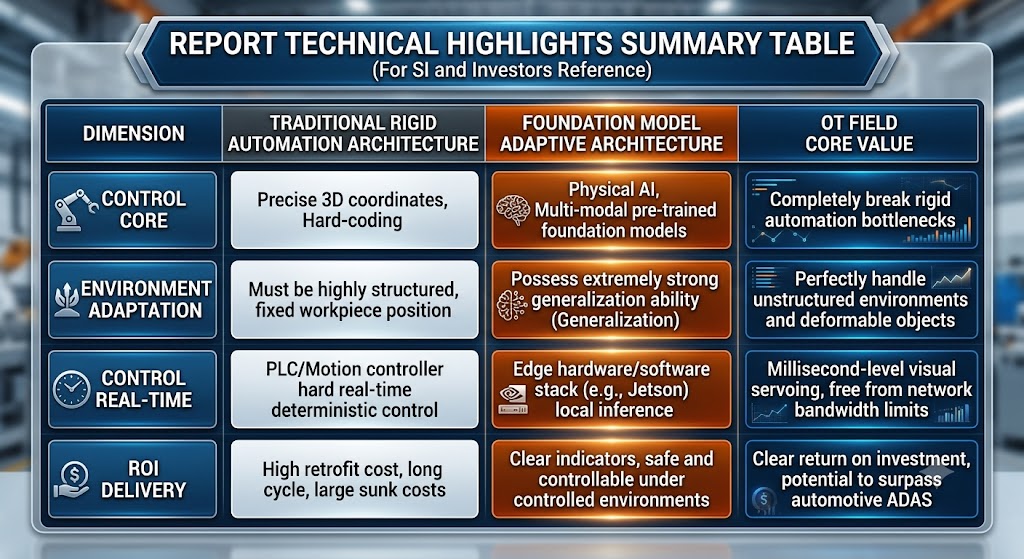

In frontline factory operations, chief engineers and factory managers have long faced a dilemma: on the one hand, ever-increasing labor costs and a growing shortage of skilled workers; on the other hand, the inability of traditional industrial automation solutions to cope with unstructured environments. Existing industrial robots and automated production lines essentially execute pre-defined control logic within a highly deterministic space.

However, when faced with the need to handle deformable objects of varying shapes and materials, or frequently changing flexible production demands, the limitations of traditional systems become glaringly apparent. This type of automation, driven by precise three-dimensional coordinates and hard-coded logic, is known as "rigid automation." Once operating conditions deviate from preset parameters, the system frequently malfunctions, leading to significant unplanned downtime and directly reducing overall equipment efficiency (OEE).

According to an official report released by ABI Research, advancements in physical artificial intelligence technology are breaking through this bottleneck. The global market for basic robot models is projected to reach $150 billion by 2036. This figure not only signifies the birth of a new technology market but also indicates that automation technology is transcending the boundaries of traditional industrial robots, deeply penetrating labor-intensive industries such as manufacturing, warehousing and logistics, healthcare, and retail/food service.

II. Paradigm Shift: Breaking Hard-Coding Limitations and Introducing Generalization Capabilities

To understand the profound changes brought about by this technology, it is essential to clarify the fundamental difference between "Robotics Foundation Models" and hard-coding in traditional control engineering. Traditional robotic arm programming relies on precise trajectory planning. Control engineers need to use teach pendants or offline programming software to specify strict X, Y, Z coordinates and Euler angles for the robot. In this mode, the robot lacks "understanding" and "perception" of its environment; once the workpiece's position shifts or its shape deforms, the robotic arm cannot accurately grasp it.

The core of Robotics Foundation Models lies in the introduction of generalization capabilities. It is pre-trained using massive amounts of multimodal data, integrating visual perception, force feedback, and control commands into a single end-to-end network architecture. The foundation model no longer focuses on absolute geometric coordinates but learns the general physical laws governing object manipulation. This enables robots to learn, reason, and manipulate various unstructured, deformable objects with unprecedented robustness.

In real-world industrial settings, this means that system integrators (SIs) no longer need to design extremely complex rigid fixtures or write thousands of lines of conditional statements when facing traditional challenges such as fabric sorting, food packaging, or wire harness assembly. Instead, robots can automatically adapt to changing working conditions by utilizing the zero-shot or few-shot learning capabilities of a basic model. This evolution from "precise programming" to "adaptive generalization" represents a significant paradigm shift in industrial automation control logic.

III. Scenario Implementation and Market Landscape Breakdown of Four Major Sectors

ABI Research data clearly depicts the commercial landscape of adaptive control technology in major labor-intensive industries over the next decade. Due to varying degrees of urgency in reducing labor costs and operational flexibility across different industries, the underlying business drivers for its implementation also differ: Manufacturing (Largest Recent Growth Driver: $30 Billion):

Manufacturing (Largest Recent Growth Driver: $30 Billion): In traditional discrete manufacturing, shortened product lifecycles lead to frequent and costly production line modifications. By introducing an adaptive base model, robotic arms can handle different types of workpieces on mixed lines, significantly improving OEE (Outcome Effectiveness) and achieving perfect compatibility with existing equipment, enabling "reuse and smooth upgrades" of production lines.

Warehousing and Logistics ($21 billion): Logistics centers face the challenge of handling massive numbers of random SKUs. Traditional vision systems are prone to failure when dealing with disordered palletizing and piece picking. The base model gives mobile robotic arms extremely high robustness, eliminating blind spots in vision and motion planning during mixed and disordered grasping.

Healthcare ($16 billion): In flexible hospital supply delivery, sterile instrument loading and unloading, and high-precision assisted applications, high reliability and sensitivity to environmental perception are bottom-line requirements. Adaptive control significantly reduces the system's false alarm rate.

Food, Retail, and Hospitality ($27 billion): These industries have extremely high staff turnover. Replacing basic repetitive labor with more powerful robotic systems can fundamentally hedge against the business risks caused by labor shortages while maintaining operational flexibility.

IV. The Behind-the-Scenes Computing Power Game: A Collaborative Ecosystem for Edge Hard Real-Time and Cloud Lifecycle

Industrial applications differ fundamentally from internet applications, placing stringent demands on hard real-time and deterministic control. In the world of PLCs or motion controllers, millisecond-level jitter can lead to mechanical collisions or product failure. Therefore, the deployment of large-scale models cannot rely entirely on cloud computing; the focus of the computing power game inevitably lies in edge deployment.

Currently, chip and cloud giants are building a clear edge-cloud collaborative ecosystem based on the actual needs of control engineering:

NVIDIA's Position on the Device Side: NVIDIA currently holds a significant leading position in the field of device-side robotics computing with its Jetson platform. Jetson's superior hardware acceleration capabilities enable local inference latency for large neural network models to be compressed to within milliseconds, meeting the stringent requirements of robot visual servoing and real-time trajectory correction, and ensuring the system is unaffected by network bandwidth limitations or sudden network outages.

The Counterattack of Edge Hardware and Software Stacks: Faced with Nvidia's dominance, competitors such as Intel, AMD, Qualcomm, and Ambarella have not stood idly by. They are actively building alternative edge hardware and software stacks. For example, Intel is enhancing the deterministic latency performance of its edge computing chips in heterogeneous computing; Qualcomm and Ambarella, leveraging their expertise in low-power, highly integrated embedded vision chips, are striving to gain market share in the mobile robotics (AMR) and drone markets. This competition provides system integrators with richer possibilities for reusing existing and customized hardware and software combinations.

Backstage Support from Cloud Service Providers: Cloud giants such as AWS, Microsoft Azure, and Google Cloud position themselves within the backstage ecosystem. They do not directly participate in hard real-time edge control, but instead focus on supporting large-scale pre-training of models, high-performance physical simulation, and full lifecycle management (MLOps). Through millions of simulation training runs in virtual twin factories in the cloud, models already possess extremely high baseline robustness before deployment to actual production lines.

V. Commercial viability and ROI justification: Value realization in a controlled environment

From the perspective of automation industry investors, basic robot models are often compared to Advanced Driver Assistance Systems (ADAS) and autonomous driving in automobiles. However, from the perspective of commercialization and ROI, the underlying logic of the two is vastly different.

Automotive ADAS faces a completely open, dynamic public transportation environment rife with corner cases. Its safety liability boundaries are extremely blurred. To address even the 0.001% extreme operating conditions, companies need to invest immeasurable R&D costs, forcing a prolonged commercialization cycle.

In contrast, the manufacturing and warehousing logistics served by basic robot models belong to typical controlled environments. In this environment, although the manipulation challenges posed by unstructured objects still exist, the physical boundaries are clear, the range of operating condition changes is predictable, and safety protection mechanisms (such as safety light curtains and area laser scanners) can be strictly guaranteed through the hard locking of peripheral OT systems.

In a controlled environment, safety, repeatability, and return on investment (ROI) can be clearly and quantitatively demonstrated, allowing companies to calculate a definite profit. The reduced tooling design costs, improved OEE, and lower scrap rates resulting from the introduction of adaptive control systems can be directly translated into financial gains. Therefore, as ABI Research emphasizes, because robot models can quickly achieve ROI in controlled environments, their deployment scale has the potential to surpass that of the automotive industry in the future.

VI. Implementation Path and Industry Outlook: Smooth Evolution Based on Safety and Repeatability

For pragmatic factory managers and chief engineers, the introduction of any advanced technology cannot come at the expense of the stability of existing production systems. The initial acceleration of commercial applications will inevitably occur in the areas of collaborative robots (Cobots) and specific traditional industrial deployments.

Collaborative robots themselves possess robust collision detection and safety speed-limiting mechanisms at the hardware level. When they are first integrated with basic models, their safety risks are kept to a minimum. This combination allows operators to work alongside adaptive robots to complete complex assembly or packaging tasks, enabling gradual penetration and smooth upgrades of production lines. The experience accumulated over years of developing autonomous driving technology in areas such as safety, legal liability delineation, and multi-sensor fusion deployment frameworks will provide valuable insights for the industry in shaping its basic model deployment framework. The future factory control architecture will not overturn existing PLC and SCADA systems, but rather seamlessly integrate edge computing units carrying basic models as "advanced adaptive coprocessors" into existing control loops through standard industrial communication protocols (such as OPC UA or EtherNet/IP). This pragmatic approach of leveraging existing infrastructure for upgrades is the only acceptable evolutionary path for industrial sites.

Conclusion: The $150 billion market potential is not a phantom bubble; it is built on the real technological needs of tens of thousands of factories eager to break through rigid automation bottlenecks and improve operational flexibility. In this restructuring driven by physical artificial intelligence, only decision-makers who deeply understand edge-side hard real-time logic, grasp the ROI advantages of controlled environments, and adhere to a smooth evolution path will be able to truly transform technology into sustainable business competitiveness in the next decade.

Contact Information:

Manager: Jim Pei

Email: sales6@amikon.cn

Whatsapp: +8618020776782

Recommended Model

|

6SL3353-7AG41-7AA0 |

C98043-A7001-L2 |

790P/400/0800 ETD DC790P |

|

6SL3353-7AH41-8AA0 |

6RA8025-6DS22-0AA0 |

790/400/0037 ETD 790 |

|

6SE7038-6GL84-1BG0 |

6SE7021-8EB61 |

791P/400/0800 ETD DC790P |

|

6SY7010-0AA02 |

6SL3255-0AA00-4CA1 |

791P/400/0500 ETD DC790P |

|

6SL3352-1AE41-4FA1 |

6RY1700-0AA01 |

791P/400/0650 ETD DC790P |

|

6SL3350-6TK00-0BA0 |

6RY1807-0AA00 |

790/400/0080 ETD 790 |

|

A5E36358274 |

A5F00109409-008 |

DSQC503 3HAC3619-1 |

|

6SE7031-2HG84-1BH0 |

6SL3040-0MA00-0AA0 |

DSQC504 3HAC5689-01 |

|

MC00160783G01/F01/M01 |

6SL3120-1TE31-3AA3 |

VTA04C24 |

|

6SL3060-4AB20-0AA0 |

6SL3120-1TE23-0AA4 |

SA535689-01 F1-TPMJ |

|

6SN1118-0DM21-0AA0 |

6SA8252-0AC61 |

SA539993-02 G1-MP 11-4 |

|

6SL3130-7TE25-5AA3 |

6SA8252-0BC60 |

Hydraulic Ring VRD 350 |

|

6SL3120-2TE21-8AA3 |

6SL3120-1TE26-0AA3 |

FI830F 3BDH000032R1 |

|

6SL3351-6GE32-1AA1 |

6SE7038-6GK84-1JC2 |

FVR22LW1R-4CA |

|

6SL3351-6GE33-8AA1 |

6RY1707-0AA01 |

6ES7134-4FB00-0AB0 |

|

6SL3351-6FE33-1AA1 |

6RY1707-0AA00 |

6ES7138-4CA00-0AA0 |

|

6SL3351-6FE32-1AA1 |

C98043-A7129-L1-5 |

6ES7131-4BD00-0AA0 |

|

6SL3351-6GE35-0AA1 |

A5E03894526 PM240/340 |

6ES7135-4FB00-0AB0 |

|

6SE7090-0XX84-0BC0 |

6SE7090-0XX84-0AJ0 |

SA553657-01 C2S1 0200 |

|

6FC5357-0BB15-0AA0 |

6SL3120-1TE26-0AC0 |

TSXP572623 TSXP572623M |

|

6SN1118-0DH23-0AA0 |

6SL3120-2TE21-8AC0 |

TRICONEX AI2351 DI2301 |

New Blog

Supplyed

525011

parts to

23253

customers in

148

countries

Disclaimer:

Amikon sells new and surplus products and develops channels for purchasing such products. This website has not been approved or recognized by any of the listed manufacturers or trademarks.

Amikon is not an authorized distributor, dealer, or representative of the products displayed on this website. All product names, trademarks, brands, and logos used on this website are the property of their respective owners. The description, explanation, or sale of products with these names, trademarks, brands, and logos is for identification purposes only and is not intended to indicate any association with or authorization from any rights holder.

Powered by amikonplc.com